Strategy

Are you ready to diversify in an emerging market?

Our strategy provides exclusive access to high-yield residential projects in São Paulo through a unique partnership with market leader Vitacon. We combine this local expertise with Dutch institutional oversight from Brickfund to ensure professional management and a risk-first framework. This collaboration allows our investors to participate in off-market opportunities under the same institutional terms as global giants like Hines.

Investment Process

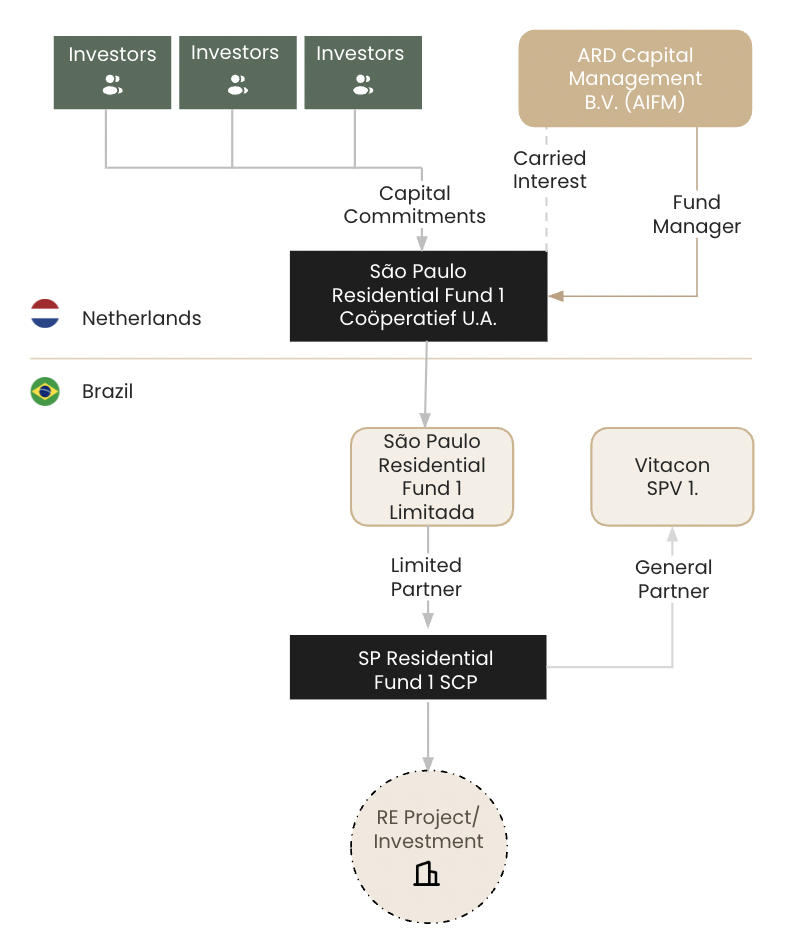

Investment Structure

AFM light cooperative

A recognized fund structure under the AFM-light regime, ensuring maximum security for investors.

Internationally recognized

An internationally recognized fund structure trusted by European, American, and LATAM investors.

Tax structure

A tax-efficient structure with the potential application of the participation exemption (deelnemingsvrijstelling).

Cup of coffee?

.svg)

.svg)

Risk Mitigation & Investor Safeguards

Project cancellation risk

If a project is not launched, the fund receives the invested amount back, indexed to inflation and increased with interest.

Developer risk

ARD’s projects utilize a performance bond with a first-rank insurer. In the event of Vitacon's insolvency, the insurer ensures the completion of the project. This serves as a completion guarantee.

Execution risk

Capital is managed via an escrow structure and only released upon achieving set milestones and through continuous monitoring.

Capital structure risk

Changes to the capital structure or governance are only possible with the fund's prior written consent.

Our Fee Structure

ARD’s fee structure is centered around transparency and a long-term vision. ARD co-invests under the same conditions as its investors, ensuring maximum alignment. The fund utilizes a compounded hurdle of 10% per year, which aligns with how wealth and benchmarks grow and provides a fair representation of returns. While many funds use a non-compounded hurdle to their own advantage, ARD deliberately avoids this. ARD only receives 20% of the additional return in cases of structural outperformance above 10%. The fees are fair, transparent, and focused on collective long-term value.

1.5%

1%

10%

20%

ARD vs. Traditional Asset Classes

Unlike traditional funds that lock up capital for years, we leverage São Paulo’s high demand to deliver immediate liquidity. Because projects often sell out within months due to strong pre-sales, we generate early cash flow that allows for a monthly interest component of approximately 1% during the development phase.

This structure provides a secure bridge to a projected 25%+ net IRR, protected by Dutch AFM-light oversight and insured completion guarantees.

Got Questions?

Our investments and operations are based in Brazil, meaning the underlying assets are valued in Brazilian Real (BRL). Consequently, the final return converted back to Euros is exposed to EUR/BRL exchange rate movements. While Brazil has an autonomous Central Bank managing its monetary policy and currency stability, investors should factor in standard currency fluctuation risks when evaluating their expected returns. This can be positive or negative.

As with any dynamic market, inflation is a standard economic factor. Brazil’s Central Bank actively monitors and responds to inflationary pressures, with current forecasts around 4.5% to 4.7% for 2025 and 2026. While real estate often moves in tandem with inflation, sudden or prolonged inflationary spikes can impact construction costs and local purchasing power, which are inherent risks in the development process.

Brazil operates as a mature democracy with established legal frameworks and maintains a neutral stance in global trade, making it a key partner for Europe and the US. However, investing internationally always involves exposure to local macroeconomic and political dynamics. Changes in government policies, local tax structures, or economic regulations are systemic risks that can influence the broader real estate market.

Our rapid pre-sale development model involves several standard real estate and cross-border risks:

Completion Risk: The inherent risk associated with any construction phase, including potential delays, supply chain disruptions, or cost variations during development.

Liquidity Risk: Real estate is an illiquid asset class. While our model focuses on generating cash flow during development, the invested capital remains tied up for the duration of the project cycle.

Regulatory & Legal Risk: Operating internationally requires adherence to both Brazilian and European financial frameworks, which are subject to potential legislative changes over time.

Market Risk: General market dynamics and consumer demand can fluctuate, which may impact the sales pace of the units and the overall project returns.

Our core exit strategy is driven by the pre-sale of developed real estate units, a model designed to generate structural cash flow throughout the construction phase. The primary risk to this strategy is a potential market slowdown, which could affect the anticipated sales pace or final unit prices. Furthermore, finalizing the exit involves repatriating capital and profits from Brazil to Europe; this process is subject to international transfer regulations, prevailing market conditions, and exchange rates at the time of the transfer.